When Bitcoin emerged in 2009 from the turbulence of the world financial crisis, traditional financial institutions simply ignored it, while a few considered it pretty ordinary: a peer-to-peer electronic payment system introduced by an unidentified author Satoshi Nakamoto through an academic white paper. Many regarded the fundamental value of Bitcoin as zero. It took almost over a decade for those who disregarded crypto to understand the underlying value when the “market value” of cryptocurrencies crossed over $3 trillion in 2021, and bitcoin price was at an all-time high of $68,789.63.

While all these years, this revolution was primarily led by retail investors. Over 300 million people own crypto globally, with wild tales of fortunes made. A tremendous shift in the investment pattern was witnessed globally. More than 19,000 cryptocurrencies have been launched and are currently in use. As all these developments were happening at lightning speed, the traditional financial players could no longer afford to put them aside.

While we know what drove traditional intermediaries, like banks and investment funds, to take on exposures in the crypto market, how big is their position there? How significant are new intermediaries like cryptocurrency exchanges? With the FTX crisis, the debate is again back – this time not on crypto but on the centralized exchanges that facilitate investments and trading. Will it slow down or halt institutions’ interest?

Progress so far: Adoption

Many leading institutions have already begun adopting crypto, especially in the US, where Wall Street is increasing its cryptocurrency offerings in wealth management, trading, and investment banking after years of resistance. On the Chicago Mercantile Exchange, one may trade futures and listed options for a number of well-known digital currencies. In March, Goldman Sachs conducted its first over-the-counter Bitcoin options exchange. In the meantime, many asset managers are preparing cryptocurrency funds to meet demand from younger, savvier investors. BlackRock participated in a $400 million fundraising round in stablecoin issuer Circle last month.

In the Crypto-BFSI market, every difficulty has been met with an opportunity, at least thus far. It continues to be a decentralized ecosystem that has the ability to improve the efficiency of the financial sector, even as it develops and advances toward broader institutional use.

Roadblocks and the need to tackle them

Even if the use of cryptocurrencies is constantly growing in popularity, traditional institutions are less than all to do so because they think the risks exceed any possible rewards. Despite the increasing use, banks are still cautious because they believe that dealing with these assets carries a higher risk and necessitates time-consuming and expensive due diligence.

1. Independence Nature of Blockchain Technology

Since the blockchain code and its distributed architecture are trusted rather than depending on centralized intermediaries, they don’t require middlemen and aren’t dependent on the capabilities of a centralized government, bank, or agency. The Crypto ecosystem is being developed as an alternative to traditional banking infrastructure. The central banks believe that the advent of this technology would make their presence redundant, and they won’t be able to control the money supply because of the decentralized nature of the ecosystem.

2. Customer Information and Anti-Money Laundering

Utilizing cryptocurrencies makes it possible to conduct peer-to-peer transactions without the use of a regulated middleman, allowing users to transmit money quickly and easily without having to pay transaction fees. Instead of being connected to a specific bank account or to a financial institution, transactions are merely connected to the transaction ID on the blockchain.

Also, the difficulty in tracing the crypto transactions, which could result in fraud and illicit activities on the network.

3. The volatility of Digital Assets

The price of cryptocurrencies has typically fluctuated over their brief existence. However, a number of variables, such as market size, liquidity, and the number of market participants, are the main causes of this.

Banks see this as a risk because they believe that over time, the currency may stop being a reliable investment because the price hasn’t been steady historically.

Improving the financial services

But if financial institutions are willing to adopt crypto and its underlying values, it can benefit their clients in several ways. The technology needs to be accepted by banks and treated as a friend rather than an adversary. The adoption of cryptos could tremendously improve and transform financial services.

1. Simple Onboarding & Expert Support

Banks may help the market attract less experienced or new investors by developing technologies that would make it simpler for their clients to accept cryptocurrency. Many investors do not want to explore opportunities in the crypto or decentralized finance ecosystem because these are highly technical and may be easily accessible to ing them.

Banks can simplify this by providing easy-to-use interest-bearing cryptocurrency accounts that allow consumers to invest through other financial instruments or on the back end.

2. Security of Digital Assets

Established institutions might aid in protecting digital currency from theft or hackers, relieving customers’ concerns. By placing cryptos under bank regulation, criminal activities may be reduced as well as the perception among outsiders that cryptocurrency transactions are not secure.

3. Payments Technology and Revolution

Blockchain technology offers clearing houses a quicker and more affordable replacement when processing transactions. Banking institutions might use blockchain technology to accelerate clearing and settlements.

The newfound Smart Contracts technology tracks through a computer code rather than a person’s actions; thus, the fraudulent aspect caused by intermediaries can be reduced. Banks may increase that trust by using these smart contracts as a trustworthy third party in mortgages, business loans, letters of credit, and other transactions.

By embracing cryptocurrencies and blockchain technology as a whole, Financial Institutions can go to the next level of efficiency and innovation.

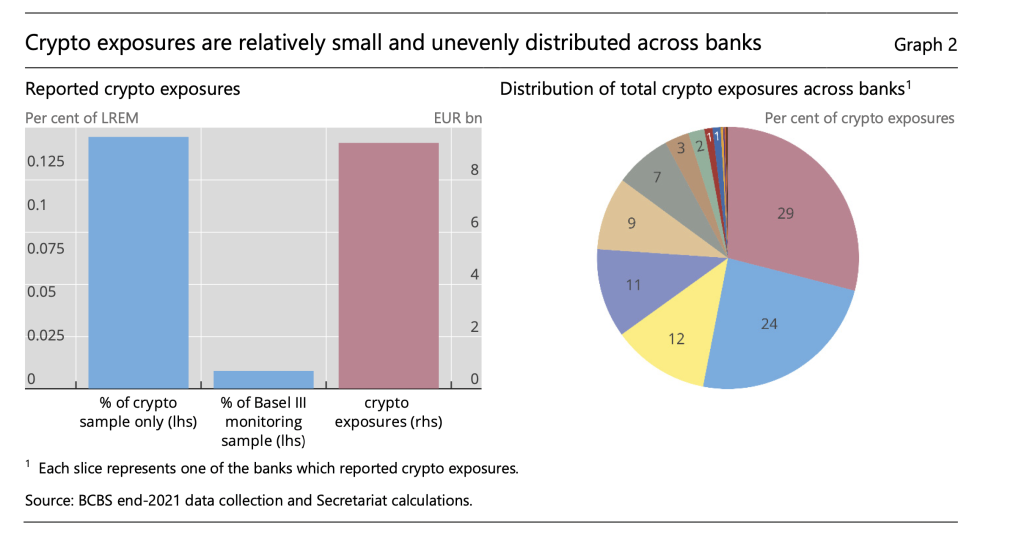

Banks’ exposures to crypto assets

Per a report by the Basel Committee, out of 19 banks that submitted crypto asset data – 10 from the Americas, seven from Europe and two from the rest of the world, a total of crypto asset exposures reported by banks amount to approximately €9.4 billion. In relative terms, these exposures comprise only 0.14% of total exposures on a weighted average basis across the sample of banks reporting crypto asset exposures.

FTX collapse ‘could delay institutional crypto adoption?

Experts believe that the FTX incident might lead to slower adoption or delayed decision as the incident has shaken up the industry’s credibility. Many have termed the collapse as crypto’s ‘Lehman Brothers moment’ while others have called it as the return of the bank run of the 21st century.

While it has been one of the most shocking news as being the second biggest crypto exchange, the news of bankruptcy impacting the fund of a million will definitely push back the progress by many years that the industry had achieved in the last couple of years.

On the other hand, it might also serve as a good opportunity for the industry to learn from its mistakes. In this context, banks and other financial institutions might greatly help crypto companies transition to matured processes and compliances, given their experience and user base.

Given the technologies and promises of decentralization these crypto ecosystems have and the large customer base and trust the banks have earned over the centuries – the combination of both can benefit users and transform the financial ecosystem profoundly.